By Giuliano Di Vitantonio, CEO, AtlasEdge

Almost 12 months ago, I became CEO at AtlasEdge, a new data centre business with a mission to create Europe’s leading Edge platform.

As anyone familiar with start-ups will know, the early days are critical. Establishing a clear, compelling vision, uniting around a common mission and, most importantly, delivering on our promises to customers.

The first chapter of our story has been marked by foresight, determination and progress. We have acquired 700+ customers across 12 countries, overseen 4 acquisitions, 1 strategic investment, and opened new offices in London and Amsterdam. We also expect to complete our acquisition of Germany’s DC1 Data Centers in the coming weeks.

I am exceptionally fortunate to be surrounded by an outstanding team and supported by our impressive shareholders, DigitalBridge and Liberty Global. With the talent, tenacity and ambition at our disposal, I couldn’t be more excited about what will unfold in 2023.

At AtlasEdge, we have an opportunity to help shape the future of Edge infrastructure and to play a small but significant part in enabling the applications of tomorrow. The shift to the ‘Edge’ is one of the most significant transitions that I have witnessed in the technology sector during the last 30 years.

As 2022 draws to a close, I wanted to share five observations from my first year at the ‘Edge’, ranging from the evolution of Edge computing applications to their impact on the underlying digital infrastructure. If you’ve read this far, I hope I don’t lose you with too much technical speak!

. . .

Observation #1: Edge computing is nothing new, but applications continue to change…

The requirement to store and process data in close proximity to where it is generated and consumed is not a novelty. However, the real-time requirements of certain applications, the exponential rise in the sheer volume of data being processed, and the associated cost of moving it across networks, are shaping an architectural paradigm shift towards more distributed data processing.

In this context, we are witnessing secular trends that are increasing the demand for Edge computing and the associated requirements on the underlying digital infrastructure:

- Applications are leveraging more ‘sensory inputs’ and are collecting data at much higher resolution and sample rates (e.g. telescopes), which exponentially increases data generation and the need for local storage and compute.

- Applications are becoming more ‘intelligent’ (e.g. autonomous vehicles), and in some cases AI requires more processing power close to where the data is generated or consumed (most frequently for inferencing but in very specific use cases also for training).

- The emergence of new applications, such as augmented reality and IoT, or new enabling technologies, such as 5G, constantly creates more use cases (e.g. metaverse and smart cities) that push the technical requirements for the infrastructure in close proximity to the end users.

- In certain use cases (e.g. online gaming and virtual healthcare), the incremental processing power is being distributed along connectivity networks, close to where the application is consumed yet not on the end user device itself. This reduces connectivity costs while improving latency and performance of data-intensive applications.

. . .

Observation #2: How the ‘Edge’ is defined varies use case by use case

In its broadest sense, Edge computing is about deploying compute capacity close to the end users, and the ‘Edge’ is the place where you deploy this processing power. Consequently, the ‘Edge’ location and its purpose will always be a function of the applications that use it.

Since each application has a different architecture, as well as a different set of requirements on the underlying digital infrastructure, how the ‘Edge’ is defined remains rather subjective and, in our opinion, unlikely to converge on a standard definition.

There was similar debate 10–15 years ago around what exactly ‘Cloud’ meant, but a clear definition has since emerged, as the technology has been deployed by cloud providers in a relatively uniform fashion. Today, the most widely adopted cloud computing architectures have converged to encompass well defined elements, such as availability zones and access nodes.

‘Edge’ will arguably have a more diversified evolution than ‘Cloud’, because each use case has a different architecture, which makes it less likely to see the emergence of a uniform approach to workload placement. As a result, we believe that the Edge infrastructure will remain more ad hoc than cloud infrastructure is today.

In particular, the location of Edge deployments will vary, with many applications being deployed in end devices, some in purpose-built technical facilities like towers and oil rigs, and others in data centres.

. . .

Observation #3: Edge computing and Cloud computing are converging

When the hype cycle about ‘Edge’ was at its early peak, it was positioned as an alternative to ‘Cloud’. Now that Edge computing is more mature and more widely adopted, it is becoming increasingly clear that these two secular trends feed off each other.

The migration of applications to the public Cloud is well underway for applications that can be deployed in a centralised location (the ‘Core’). Cloud providers are now thinking about expanding the model to more distributed applications or creating a new model, based on local zones and tailor-made for Edge computing but with similar properties to the existing one.

This complements a parallel motion to further distribute the network nodes of the hyperscalers (for capabilities such as cloud access and/or traffic aggregation/distribution, typically referred to as ‘Edge deployments’) into more and more carrier-neutral data centres closer to the end users.

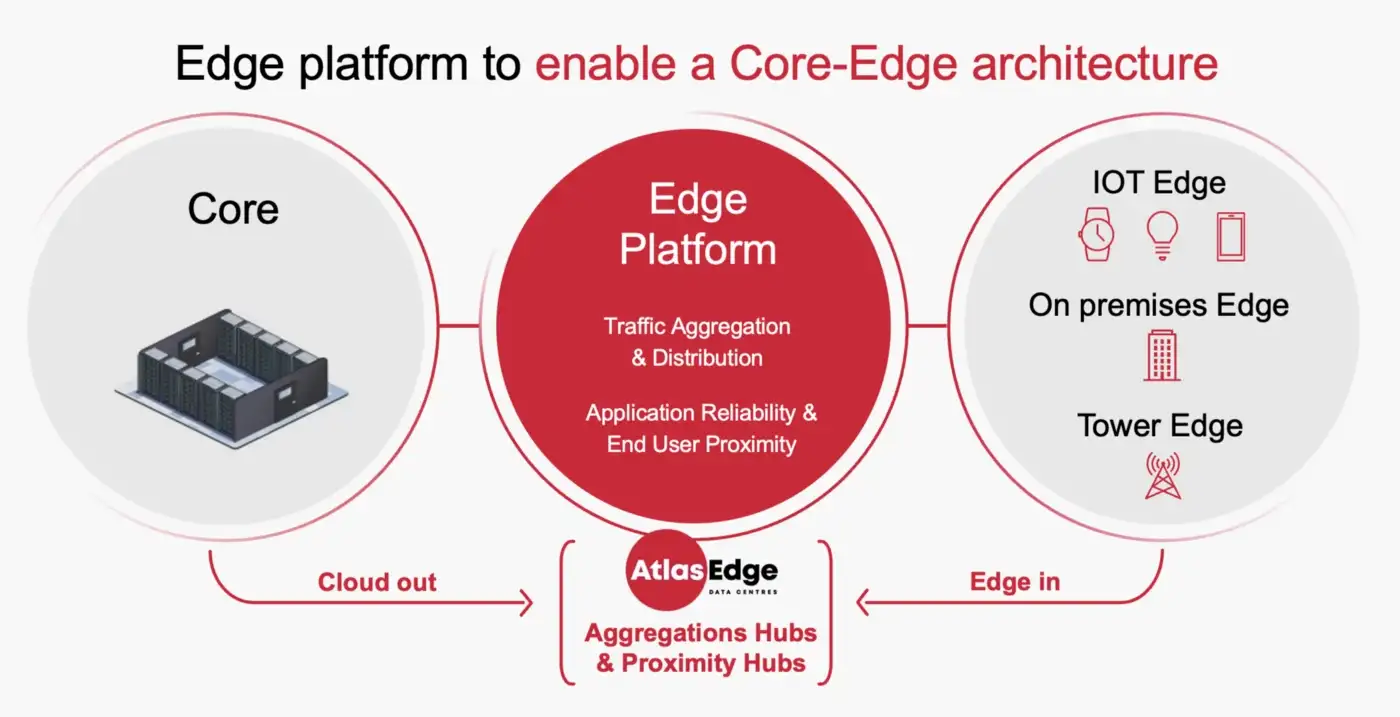

In response to this trend of geographic distribution of compute capacity and network nodes, we’ve observed a continued and significant push by the cloud providers towards more de-centralised locations (the so-called tier 2, tier 3 and tier 4 metros). We refer to this movement as ‘Cloud out’.

More recently, we have also been witnessing a complementary phenomenon, referred to as ‘Edge in’, whereby many applications which were previously sitting with the end users (either on the customer premises or in the end devices) are moving towards third party data centres that are capable of offering more availability and resiliency (and, in some cases, access to the public Cloud) but are still located in close proximity to the end users.

These two motions are rapidly converging and meeting in the middle, forming what is known as a ‘Core — Edge architecture’. This gives rise to a distributed layer of digital infrastructure that acts as a connective tissue between the ‘Core’ and end users, with Cloud providers increasingly relying on it.

. . .

Observation #4: Sustainability and data sovereignty contribute to the drive to the ‘Edge’

As technology creates growing demand for capacity in more locations, there is an opportunity to fundamentally rethink how data centres fit with the rest of the environment.

Taking compute/processing power closer to where the data is being generated has the potential to assist in improving sustainability characteristics. While massive data centres struggle to use their waste heat, there are many more potential consumers for highly distributed, high grade, locally produced heat at the Edge. Relatively small, Edge data centres, are the ideal places to deploy large scale energy storage, which will fuel the development of additional renewable generation.

At the same time, data sovereignty requirements play a role in driving a more distributed storage and processing of data. Increasingly stringent data privacy and consumer protection regulations demand that data is stored and processed within a country’s borders, or even at local level. Unlike North America, the geographic fragmentation of Europe inherently implies a far more distributed digital infrastructure, with greater emphasis placed on national and regional deployments.

. . .

Observation #5: Edge requirements are shaping the next wave of digital infrastructure

The rise of Edge computing places a new set of requirements on a global digital infrastructure that was originally developed to focus on enabling connectivity (both long haul and last mile) for enterprises and consumers, and subsequently evolved to focus on housing vast amounts of compute capacity in ever growing data centres, which became the foundation of a globally interconnected digital economy.

The fundamental driver for this new inflection point is how workload placement is shaping Edge infrastructure, with different workloads being deployed in very diverse places at the Edge of the network based on the application architecture.

As already observed, we are witnessing the emergence of a highly distributed layer of digital infrastructure that acts as a connective tissue between the ‘Core’ and the end users, with different applications being deployed in different nodes along that spectrum, depending on latency, performance, reliability, size and data sovereignty requirements.

Each node on this Edge infrastructure, be it an end user device, a purpose-built technical facility, an enterprise data centre, a colocation data centre or even a hyperscale data centre, represents a location where workloads can reside. Fibre obviously plays a critical role in connecting all these nodes together at high speed, thus enabling developers to optimise application architectures.

From a data centre standpoint, as the Edge architecture matures, we are seeing the rise of two main categories of colocation facilities bridging the gap between the Core and the end users: Aggregation Hubs and Proximity Hubs. The former are large sites used to aggregate workloads and distribute the flow of data traffic, while the latter provide a first point of reliability close to the end users. [1]

Aggregation Hubs tend to emerge naturally in locations where traffic is exchanged or large amounts of data are stored, and are currently present in 30–40 metros across Europe (but we expect this number to increase to around 100–150 over the next five years). Proximity Hubs are more application specific and are selected on an ad hoc basis, in relation to their proximity to the end users and access to the network (both local access to end users and back haul connectivity to the rest of the platform).

AtlasEdge’s mission to build Europe’s leading Edge platform is being fulfilled by providing our customers with the option to deploy their workloads in a growing number of locations across our continent.

As customers require Aggregation Hubs in a growing number of locations, we are focusing on tier-2 and tier-3 metros where the carrier-neutral options are less developed. This is where the demand for Edge deployments is happening now, and where there is the most pressing need to create ecosystems of platforms and service providers. We are also targeting tier-4 metros where, based on patterns of adoption by customers, we expect the next wave of deployments to take place, especially in countries like Germany and the UK.

At the same time, we are working closely with our most forward-looking customers on the use cases that hold the highest promise to require an even more distributed architecture, bringing a capillary network of Proximity Hubs to life. The great optionality provided by our connected footprint of real estate assets and technical facilities is the ideal foundation to pilot and refine the delivery model.

As we continue this journey with our customers, our employees, and our investors, we are aware that the coming year will have its challenges. There is real complexity in rolling out highly distributed infrastructure and adopting a replicable model which is sustainable, particularly amid a challenging macroeconomic environment marked by inflationary pressures and global supply chain complexity.

The past 12-months, however, have seen our knowledge and understanding of application requirements and customer needs at the ‘Edge’ evolve significantly. The expertise of our fantastic team goes from strength to strength, and we are well placed to continue growing our platform, expanding our footprint throughout Europe and meeting customer requirements.

Here’s to a successful 2023

[1] By definition, any Aggregation Hub can act as Proximity Hub, as long as it is in proximity to some end users.

About AtlasEdge

AtlasEdge designs, builds and operates highly secure, scalable data centres across Europe. Formed as a joint venture between Liberty Global and DigitalBridge, we’re focusing on the next wave of markets including Barcelona, Berlin, Brussels, Düsseldorf, Hamburg, Leverkusen, Lisbon, Manchester, Stuttgart and Vienna. Our proven modular-based construction enables rapid deployments under 10MW, while we continue to develop larger campuses, with a target of more than 500MW in our powered landbank.

Since 2021, AtlasEdge customers have deployed AI, cloud and mission-critical workloads in our 2N facilities, using liquid-to-chip or air-cooled designs. All new builds run on 100% renewable energy. Our tax, legal and site-selection teams also support customers entering new European regions, helping them navigate regulatory, commercial and technical requirements with confidence.